By Ewen Stewart | TCW Defending Freedom | June 27, 2022

ACCORDING TO the Cambridge Dictionary, a sanction is ‘a strong action taken in order to make people obey a law or rule, or a punishment given when they do not obey’. The purpose is pretty obvious, to try to deter an action that is not deemed by the sanctioner as acceptable.

A child thus may be sanctioned for poor behaviour with no sweets for a week. A country is equally sanctioned in some way deemed to harm the errant country and not those giving the sanction. Russia has been sanctioned by primarily the US, UK and EU in an unprecedented fashion due to the war in Ukraine. But who is it hurting?

This article is not about the morality of the situation in Ukraine. It is simply about whether the sanctions have been effective, or have they actually been counter-productive? At the most basic level, has applying sanctions made it more, or less likely, that UK policy goals will be achieved?

A third of a year into war, the only conclusion one can sanely draw so far is that the West’s sanctions have been an unmitigated disaster in self-harm undermining domestic prosperity while causing serious inflationary and monetary dislocation.

There is very little evidence that Western sanctions have materially harmed Russia’s ability to prosecute war or (as much as we can judge) diminish Russian domestic support for it. Far from Government’s expectations that it would cripple the Russian economy and perhaps lead to regime change, if anything it is Western economies that are in desperate trouble. It seems that US, UK and EU sanctions are proving to be a lose-lose trade.

A simple test – what currency traders would say

We were told sanctions were going to cripple the Russian economy and stop its war machine. For around two weeks, judging by the currency market’s reaction to a then collapsing rouble, that superficially seemed right.

Initially the rouble halved from a pre-war 75 to the USD to a low of 140 as the West confiscated over $300billion of Russia’s sovereign assets held in the West. This, coupled with a wholesale withdrawal of Western companies, from BP to McDonald’s, and a tightening of oil and gas sanctions, resulted in currency collapse.

Such a collapse, if prolonged, would have been very dangerous for Russia’s stability as it simply destroys its terms of trade, potentially resulting in material inflation as the cost of importing goods rises significantly.

But Western policy makers did not think through the second derivative which is coming back to bite. Economically Russia to an extent is the polar opposite of the West.

The West undoubtedly has significant technological and soft power advantage over Russia. However, most Western economies have growing and inefficient public sectors and weak central banking systems impeded by the Global Financial Crisis (GFC) and particularly lockdowns, with substantial growing public debt and debased monetary systems through a new-found belief in Modern Monetary Theory (MMT) – accompanied by all the associated Quantitative Easing over the last decade. Britain and the US also run substantial trade deficits.

Russia, on the other hand, is a commodity- and primary products-led export economy running a substantial trade surplus, with weak technology and service sector exports and soft power. Its public finances are very strong with low public debt, low taxes (14 per cent flat rate income tax) and substantial cash reserves even after half were sanctioned.

This asymmetry of strategic advantage between Russia and the West has profound implications if sanctions are applied. Thus quite quickly currency traders realised what extraordinarily almost none of our current crop of virtue signalling politicians dare to say – that the sanctions were potentially more of a threat to the West (UK and EU in particular) as the impact of ‘cancelling’ Russian carbon was highly inflationary.

There are no cheap short or medium term substitutes. Much of the West is dependent on Russian primary products, while only some Russians might be upset the Prada store in Moscow had closed (but the back door from China remained wide open). An inconvenience, sure; a game changer, probably not.

Thus the rouble strengthened materially and at the time of writing is 55 to the USD, almost 30 per cent stronger than before the conflict in Ukraine. If one compares the sterling- rouble exchange rate, sterling’s underperformance is even starker.

It is quite simple. Cancel Russian oil (13 per cent global production) and India joyfully buys the discarded stock at a discount while the global price goes up as the West scrambles to find new supply. Worse, cancel Russian gas and the EU has a major crisis, as does the UK given the UK’s foolish decade-plus de-emphasising of carbon, including the closure of strategic gas storage facilities. The list goes on well beyond carbon – from titanium to fertiliser, from wheat to cod.

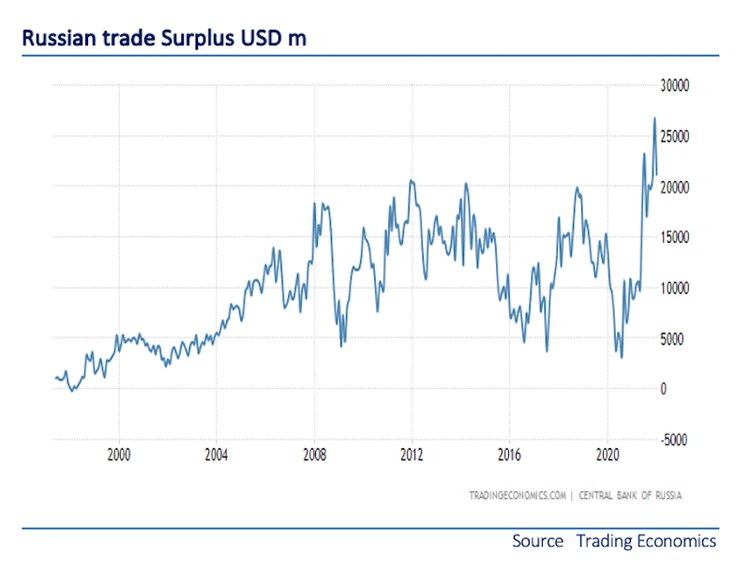

But it is oil and gas that are so critical as power is essential to the manufacture, to a greater or lesser extent, of most things. The irony is that as well as Saudi, Iran and Venezuela, the greatest beneficiary of soaring hydrocarbon prices is Russia. Putin’s Russia has run consistent trade surpluses but the current surplus is a record, as a direct result of sanctions, taking the spot price of oil from a pre-war $80 a barrel to $120 today.

While the rouble strengthens and the Russian trade surplus expands, the effect on Western economies has been devastating. In fairness the West had been severely undermining its own advantage for many years prior to the invasion of Ukraine, fuelled by Governmental policies based on a double fallacy: that monetary policy could solve all ills, and that centralised decision-making and excessive public spending could solve all ills.

Both fallacies are now coming with a substantial price, but to multiply that with an ill-thought-out sanctions regime that is achieving none of its underlying goals and is harming Western economies is frankly hard to fathom.

The West, particularly the EU and UK, is now in a pickle. This pickle has the potential to be calamitous as Governments remain in denial at the scale of the challenge they are facing.

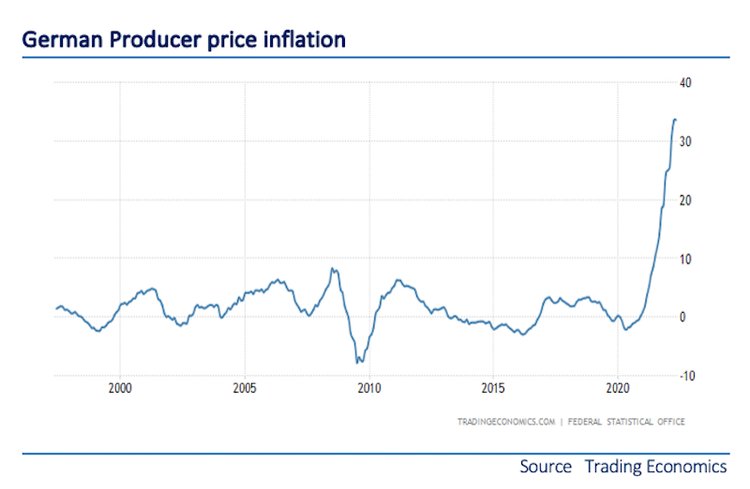

We are in a situation where the inflationary surge, given supply chains, is in its embryo stage, not close to its conclusion. Sure, the price rise at the pumps is immediate, but domestic energy prices are set to increase by a further 40 per cent in September when the price cap comes off. As a warning, German producer price inflation (see chart below) is over 30 per cent, a rate not seen since post-war ruination in 1946.

I sincerely hope I am wrong but this has the potential to get very nasty. Rishi Sunak said on Wednesday: ‘We are using all the tools at our disposal to bring inflation down and combat rising prices. We can build a stronger economy through independent monetary policy, responsible fiscal policy which doesn’t add to inflationary pressures, and by boosting our long-term productivity and growth.’ That says to me he hasn’t a clue about the scale of the challenge or indeed the underlying causes.

The reality is unfortunately that both the Bank of England and the ECB are so far behind the curve as to make you weep. Interest rates of 1.25 per cent when RPI is 11 per cent are so far off-kilter while the ECB, with arguably an even greater inflation headache given German industrial reliance on Russian gas, is only now coming off negative rates.

Moreover, expanding a wantonly inefficient public sector to around half the entire economy coupled with an unprecedented regulatory stranglehold can only spell a productivity disaster. It is throwing money at the bad, paid for by the good.

Where this will end remains uncertain, so many unknowns are there. What we can predict is that this is the beginning not the end of the maelstrom. Governments do not like short-term pain as elections approach and we risk yet another debt-funded stimulus papering over the ever-wider cracks. How credible would that really be when inflation is 11 per cent? Would they dare print money again in such circumstance? I fear they would.

This country and indeed Europe generally is enduring enormous self-harm. Sanctions have backfired but the cocktail of sanctions, massive public sector expansion, delusional monetary policy and delusional energy policy risk an economic disaster of immense proportion.

There is no easy fix but unless we wish to become a northern version of Argentina, with a debased currency, constant crisis and missed opportunity, we need to understand the scale and multiple layers of our challenge.

It’s too late to avoid prolonged and meaningful inflation, and in time recession, but it’s not too late to start to rectify policy error. I can’t see the current crop of politicians analysing forensically the impact of sanctions but a great start would be to toss away the gateway drug to our delusions, the strange idea that Modern Monetary Theory works and governments can print and spend their way out of a crisis. Frankly they can’t and with that acceptance perhaps we can start the process of an appropriately balanced economy focused on private activity, not state direction. Government got us in this mess, only the people can free us from it.

Leave a comment